For 3 months, they were almost inseparable. Then in June, they went their separate…

What’s the Best Way to Improve Your Credit Score for a Mortgage?

Why should you improve your credit score?

Improving your credit score for a mortgage can be one of the most efficient ways to improve your monthly payment, interest rate, and borrowing costs without making a huge down-payment.

Qualifying for a mortgage can be a difficult process even for borrowers who have stellar credit. The process becomes even more daunting when credit scores aren’t great. Not only is the process more difficult for borrowers with lower credit scores, but mortgage interest rates and borrowing costs can be much higher, too.

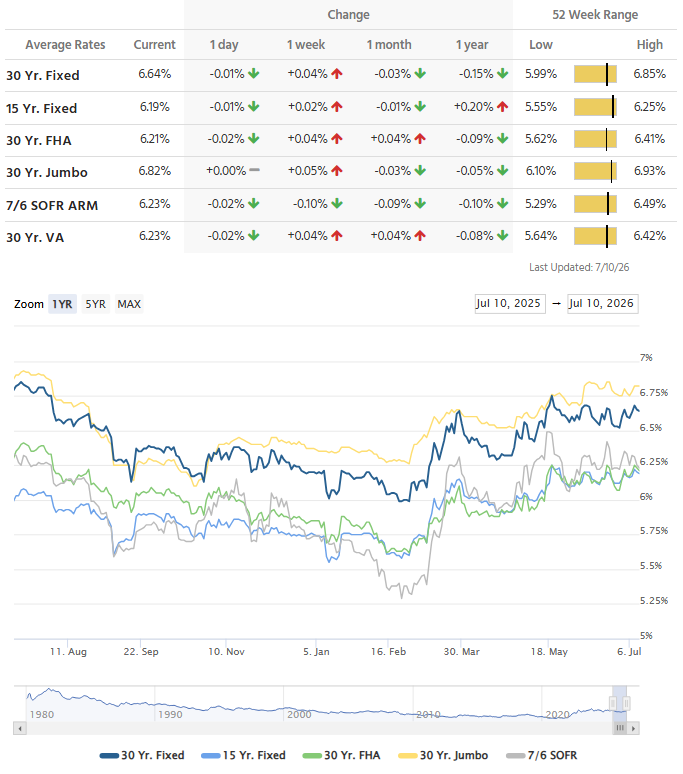

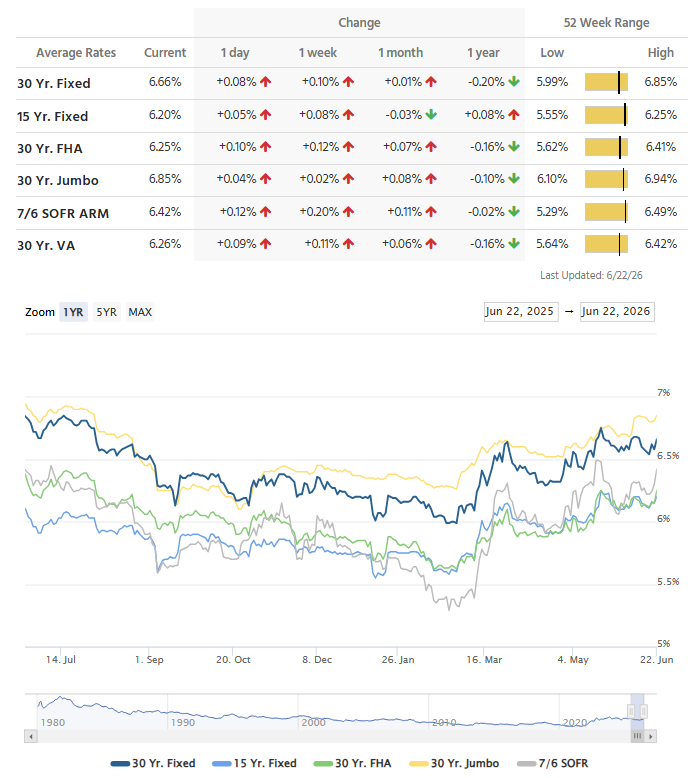

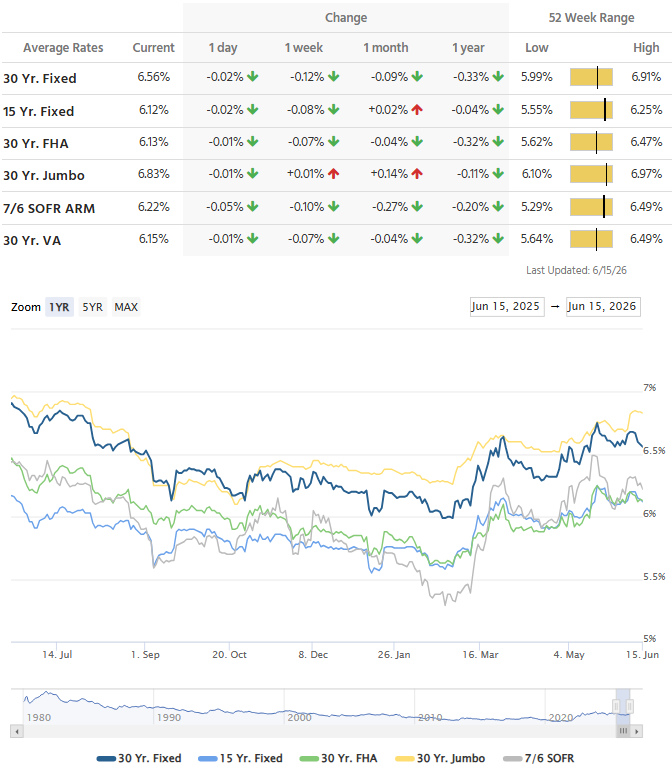

As an example, here is a comparison of today’s interest rates for a $250,000 conventional mortgage purchase with 5% down on a primary home in Brunswick, Georgia:

-

740+ Credit Score

Rate: 3.375%

P&I Payment: $1,050

-

700 Credit Score

Rate: 3.75%

P&I Payment: $1,117

-

660 Credit Score

Rate: 4.625%

P&I Payment: $1,221

-

620 Credit Score

Rate: 5.25%

P&I Payment: $1,311

As you can see, the cost to borrow money rises quickly as credit scores drop. Not only do mortgage interest rates increase, but private mortgage insurance rates on conventional mortgages also increase as your credit score decreases, compounding the cost even further!

So, what’s are some of the best ways to increase your credit scores? Here are a few:

-

Pay Down Credit Card Balances: Any balance over 30% of the credit limit will reduce your score. Keeping your balances below 30% (10% is the magic number) will help your scores improve immediately. You can also ask your creditor to increase the credit limit on your account to reduce the usage without paying the balance down.

-

Reduce Credit Inquiries: Any credit inquiries within the past 120 days can drop your score slightly, but multiple credit inquiries for different types of credit will drastically reduce your score. Try to refrain from applying for credit prior to applying for a mortgage.

-

Get Added to Someone’s Credit Card as an Authorized User: If you have a spouse, relative, or friend who has excellent payment history on a credit card with a low credit usage ratio, ask to be added as an Authorized User. This will immediately give your credit a boost by adding their payment history to your credit history.

-

Have Collection Accounts Removed: This can be difficult, but having collection accounts deleted from your credit report can increase your score by 100 points or more. Contact the creditor and ask how you can get a Letter of Deletion before you pay off any balance. Just one $25 collection account can drop an 800+ credit score into the low 700s.

-

Correct Errors on Your Credit Report: Always use a credit monitoring service to keep track of your credit report, and dispute items that are incorrect. You can view what Transunion, Equifax, and Experian have on file for you once a year at www.annualcreditreport.com , but I also recommend using Credit Karma to see where your scores are trending. You won’t get actual mortgage credit scores with Credit Karm, but you will get a good feel for where you stand, and see if your efforts are improving you scores.

At Capital City Home Loans, I have the ability to perform a manual rescore of your credit that only take 3-5 business days. If you need help improving your score, or would like a recommendation for a credit repair company, please contact me today.

Improving your credit score will reduce your interest rates and cost to borrow money with credit cards, car loans, and any other type of financing you might need.

Related Posts