For 3 months, they were almost inseparable. Then in June, they went their separate…

2022 Year End Mortgage Rate Update

The last 2 weeks have mostly uneventful from a market news standpoint, but rates have crept up slowly.

Check out my video above for an update on the past week’s movement and this week’s potential market movers.

Where Are Mortgage Rates This Week?

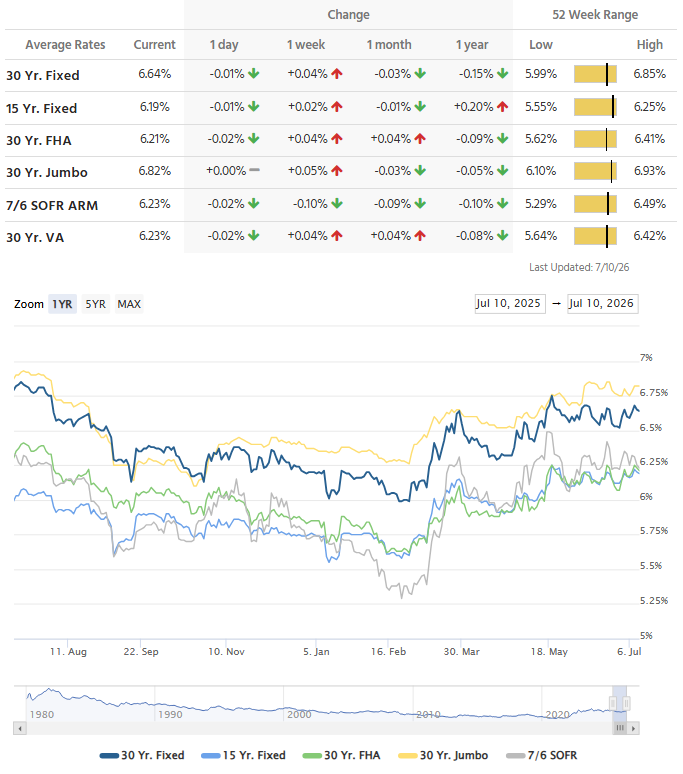

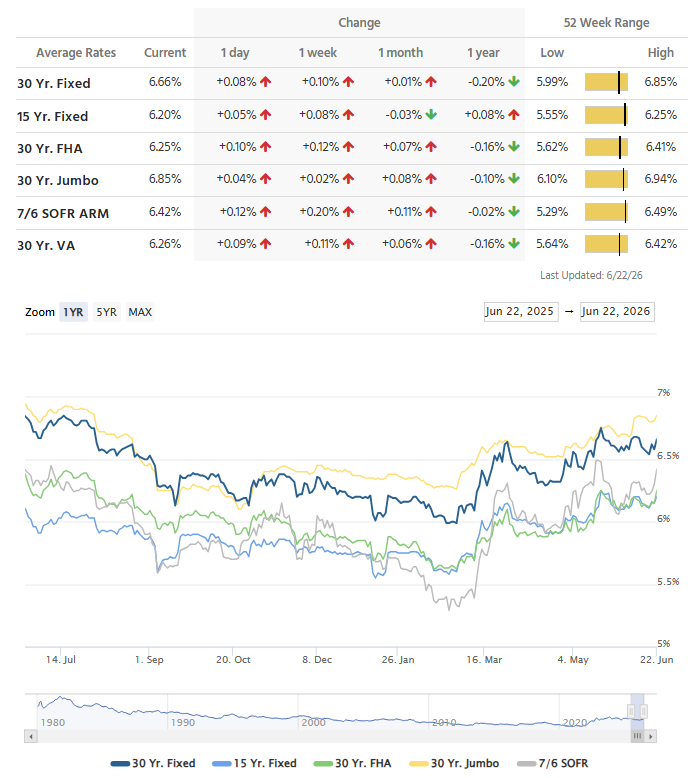

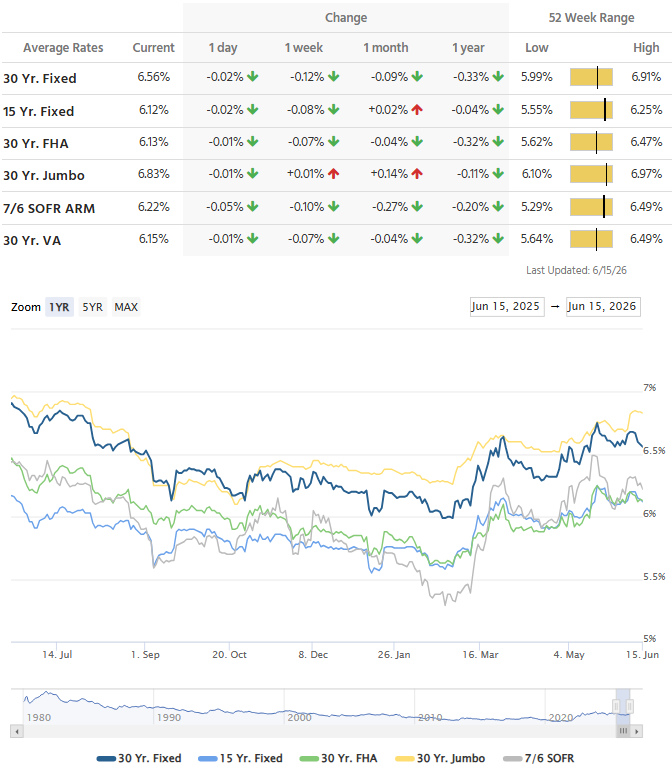

Average 30 year conventional fixed rates for excellent scenarios with a 1 point discount charge are right around 6.375% (6.500% APR) with 15 year rates around 5.50% (5.625% APR). These rates are 0.125% higher for 30 year notes and flat for 15 year notes compared to our last update.

It’s worth noting that rates with no discount points have moved higher more quickly to around 7.00% on 30 year fixed rate notes.

If we look at rates on a year-to-year basis, rates are a little over double what they were on December 31st, 2021 – a change from an average of 3.375% to 7.00% with no discount charges on 30 Yr fixed rate mortgages.

What’s Moving Markets?

Bond traders are mostly on holiday mode and have been since before Christmas. Light trading paired with sparse economic news during the holidays has kept rates mostly stable the last couple of weeks. Bond traders work a full day today, and a half day on Friday before closing for a 3 day weekend (those that aren’t already on vacation, anyway). I don’t expect to see much movement in rates until everyone gears back up mid-week next week.

Up until just the past few weeks, the go-to headline to quantify the pace of recent mortgage rate movement tended to reference rates being the lowest in several months. Now at the end of December, the average lender is up to levels not seen since the end of November. Granted, we have a few days to go before officially declaring the highest rates in a month, but being at the highest rates in 28 days still isn’t the greatest news.

Even then, we really haven’t seen any truly traumatic spikes in the past 2 weeks. It’s been more of a steady march serving as a correction to what were perhaps overly optimistic levels in mid December.

The results may or may not look anything like the 2nd week in January. Fortunately, we can be fairly confident that day-to-day rate movement will be much more willing to respond to economic data at that time. So even if rates do remain under upward pressure, it would at least be much easier and more logical to reconcile while that’s happening.

The Pending Home Sales report from NAR showed a 4% decline in November back to levels not seen since the pandemic shutdown in April of 2020. It also brings the index below the lowest level seen after the Great Financial Crisis.

But at this point, does an additional dose of weakness change the bigger picture? Not really. Being able to say “existing home sales fell below 2010’s lows” would just be a talking point and another way to state what’s already obvious. Home sales are searching for a floor. We’ll know it when we see it. Until then, we can only hope and assume that some relief in the form of lower mortgage rates and more even-keeled inflation would help both the demand and supply sides of the home sales equation.

NAR’s Lawrence Yun notes “There are approximately two months of lag time between mortgage rates and home sales. With mortgage rates falling throughout December, home-buying activity should inevitably rebound in the coming months and help economic growth.”

Related Posts