Highest Rates in Over a Year (And a Small Recovery) While the milestones may be significant,…

Weekly Mortgage Rate Update

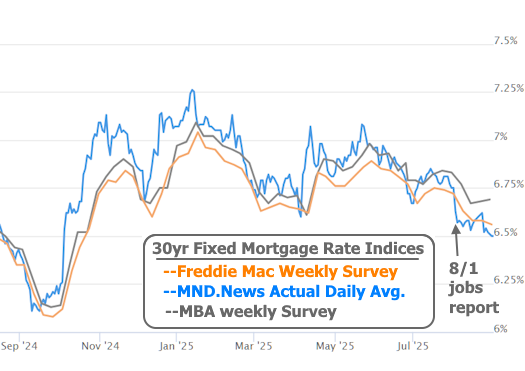

Calm Before the Storm: Rates Drift to 11-Month Lows Ahead of Critical Jobs Report

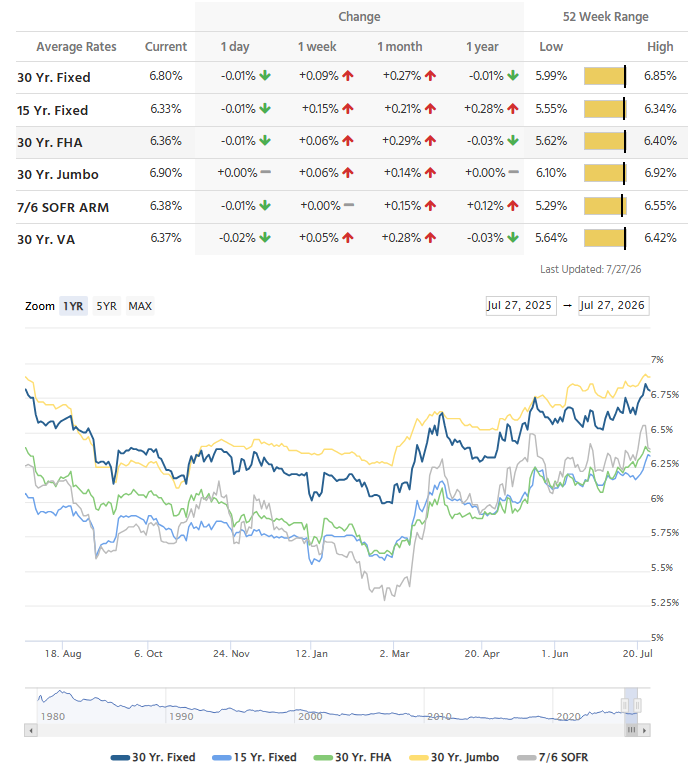

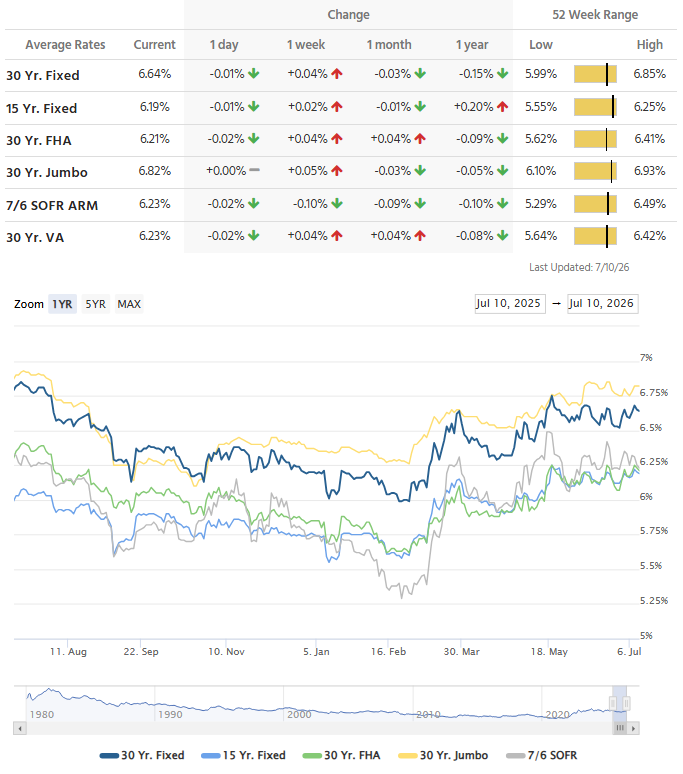

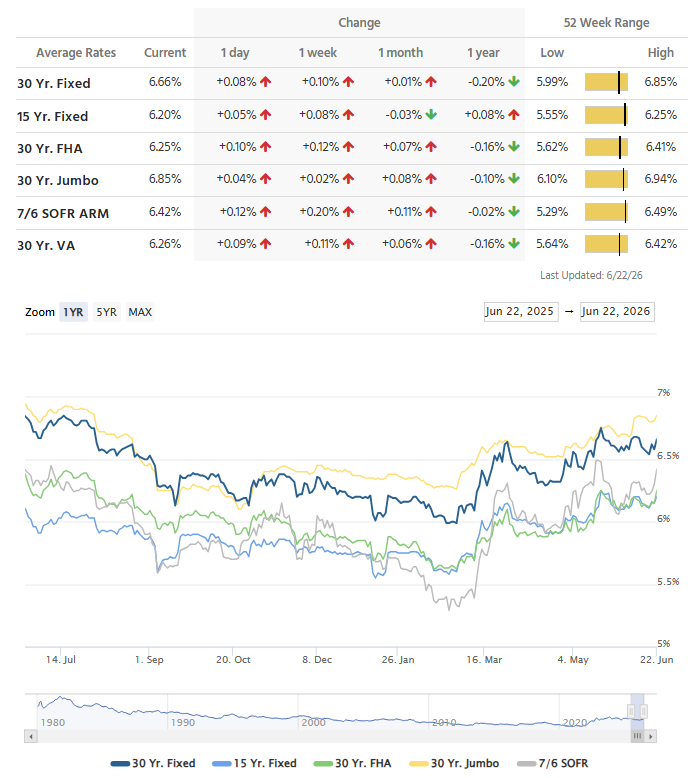

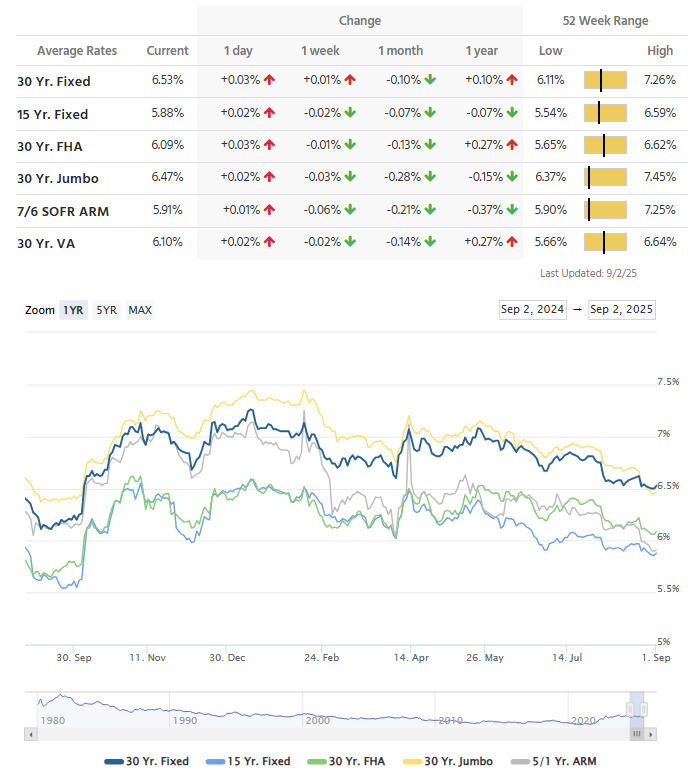

National Mortgage Rate Survey

Data Source: Mortgage News Daily

*Rates can vary significantly with different creditscores, down-payments, property types, and a variety of other factors. The below are all based on best-case scenarios.

This is not an offer to lend. This is a rate survey published by Mortgage News Daily. Ask your clients to get an official Loan Estimate before making a decision.

The MND Rate Index is the best way to follow day-to-day movement in mortgage rates. Their index is driven by real-time changes in actual lender rate sheets. This has two huge advantages compared to the Freddie Mac survey – timeliness and accuracy. Call me anytime for an update.

This past week was a classic placeholder for mortgage rates. With no big-ticket reports on the calendar, volatility stayed about as low as it gets. But even without fireworks, the market quietly added up small, steady improvements each day, ultimately pushing rates to their lowest levels since October 3rd, 2024.

Each move was subtle. Rates never moved more than 0.02% on any given day. That’s small enough that most borrowers wouldn’t notice any change in rate quotes from one day to the next. But the small changes were all “victories,” technically. And they added up. MND’s index of top tier conventional 30yr fixed rates is now 6.50%, the lowest in nearly 11 months.

In many ways, the lower rates are simply a continuation of a trend that began with the surprisingly weak jobs report on August 1st. That report, and the subsequent revisions to earlier months, reset expectations about the labor market and the Fed’s next moves. Mortgage rates got most of the way to current levels by the following business day (as seen in the chart above).

Unlike the one we just lived through, this week’s calendar is packed with high-stakes reports. The jobs report on Friday is always the main event, but it won’t be alone. All four trading days (markets are closed Monday for Labor Day) carry economic updates with market-moving potential. Some market watchers are even giving more weight than usual to Wednesday’s ADP private payrolls report. That’s not because traders have suddenly lost confidence in the government’s jobs tally, but rather because two months ago ADP correctly flagged a significant slowdown in payroll growth that was only confirmed later by revisions to the official data.

Bottom line: we just enjoyed one of the calmest, friendliest weeks for rates in 2025 so far. Don’t expect that calm to last. By Friday, the conversation could look very different depending on how the jobs data shakes out. This isn’t to say this week will necessarily be unfriendly, simply that it has much more potential volatility, for better or worse.

Related Posts