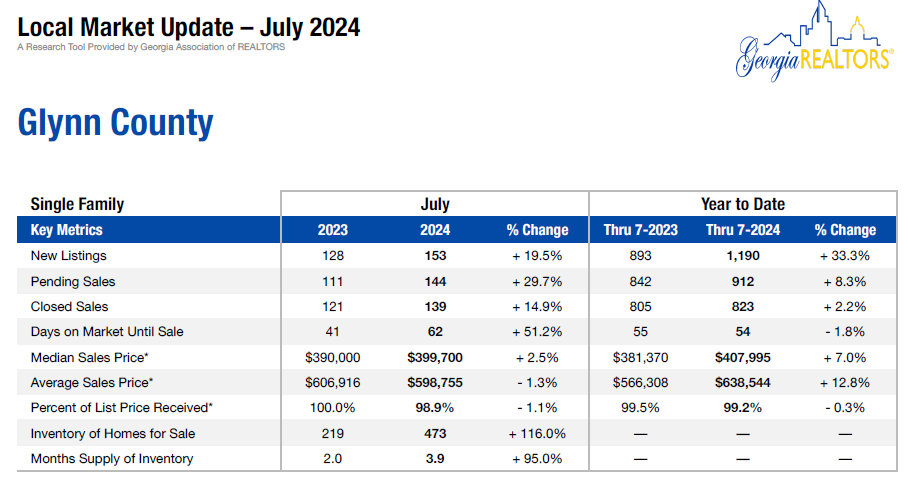

Glynn County July Housing Market Update: Navigating a Changing Landscape Glynn County, Georgia, with its…

Top 10 Mortgage Credit Do’s and Don’ts

Mortgage credit can be a tricky thing to navigate. Good credit is critical when it comes to obtaining the best interest rates on terms on a mortgage. Here are the top 10 mortgage credit do’s and don’ts when looking to secure a mortgage to purchase your next home or refinance your existing home:

Mortgage credit can be a tricky thing to navigate. Good credit is critical when it comes to obtaining the best interest rates on terms on a mortgage. Here are the top 10 mortgage credit do’s and don’ts when looking to secure a mortgage to purchase your next home or refinance your existing home:

- Do NOT apply for new credit or allow any company to check your credit. New inquiries can reduce your score and raise your debt-to-income ratio. If you have to get a credit check with a utility company, please let your mortgage banker know ahead of time and he or she can take care of that. At best, new inquiries will cause you to have to produce more paperwork and documentation. At worst, they can cause the loan to be denied.

- Don’t pay off collections or charge-offs unless instructed to do so. If you are requested to do so, request a “letter of deletion” from the collection agency BEFORE you pay them off. A paid off collection account that remains on your credit report with a zero balance can sometimes cause your credit scores to drop.

- Don’t close credit cards. This can lower your credit score by reducing your average age of accounts and increasing your debt usage ratio.

- Do not max out credit cards. Try and keep the balance less than 30% of the total credit limit. 10% seems to be the “perfect” credit usage ratio for the highest credit scores.

- Do not consolidate debt onto one credit card. It could make you appear “maxed out”. This can raise your minimum monthly payments and lower you credit score. Higher payments could potentially raise your debt-to-income level and cause your application to be denied.

- Do not add new accounts, co-sign a loan with anyone else or get added as an authorized user.

- DO make all your current payments on time. One 30 Day Late payment can cost you the mortgage!

- Do not quit or change jobs! You’d be surprised how often that happens and it can and will derail a mortgage application.

- Do not make any large deposits into or withdrawals from any of your bank accounts. If you really need to do so, contact your mortgage banker to discuss your options. Large deposits must be sourced and can cause major problems if the money can’t be sourced easily.

- DO call me with any questions about these items!

This is not a definitive list, so just remember than any change in your financial picture can affect your mortgage credit including credit accounts, bank statements and job status can derail the mortgage process. As your lender, I will work hard to make sure the mortgage process is as smooth and as stress-free as possible. By following these guidelines before and during the mortgage application process, your new home purchase or refinance will be much more pleasant!

Please call me today at 912-638-3005 or Apply Online so we can discuss your financial goals and get you ready to buy your new home or refinance your current home and save some money!

Related Posts