For 3 months, they were almost inseparable. Then in June, they went their separate…

The Fed is Cutting Rates, But Not Mortgage Rates!

The Fed is Cutting Rates, But Not Mortgage Rates!

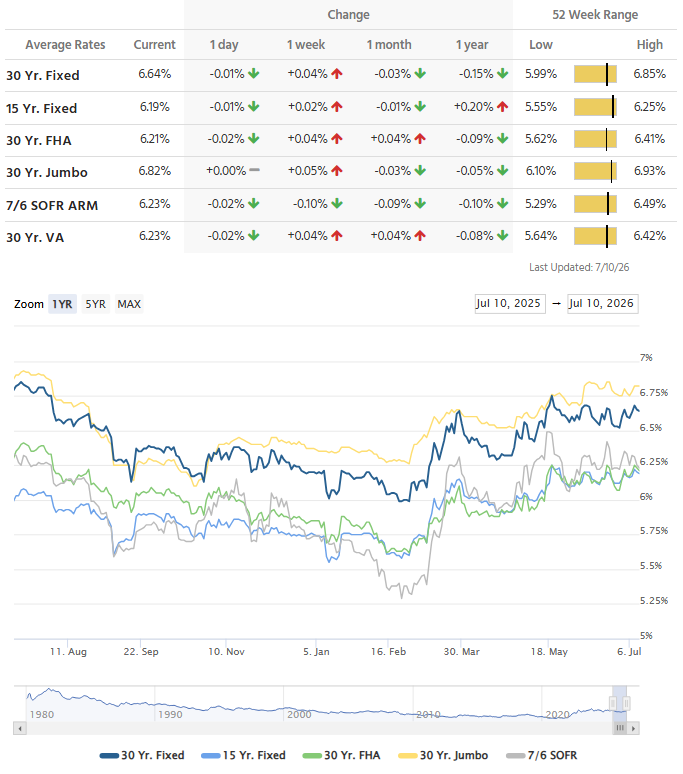

National Mortgage Rate Survey

Data Source: Mortgage News Daily

*Rates can vary significantly with different credit scores, down-payments, property types, and a variety of other factors. The below are all based on best-case scenarios. This is not an offer to lend. This is a rate survey published by Mortgage News Daily. Get an official Loan Estimate before making a decision.

The MND Rate Index is the best way to follow day-to-day movement in mortgage rates. Their index is driven by real-time changes in actual lender rate sheets. This has two huge advantages compared to the Freddie Mac survey – timeliness and accuracy. Call me anytime for an update.

The Fed is Cutting Rates, But Not Mortgage Rates!

The end of October brings the next Fed announcement and it is a 100% certainty that they will be cutting rates again. Many people believe this means lower mortgage rates.

Many people are wrong.

To be perfectly fair, mortgage rates COULD move lower after the Fed rate cut, but they could also move higher. We’ve certainly seen our fair share of counterintuitive reactions to rate cuts in the past.

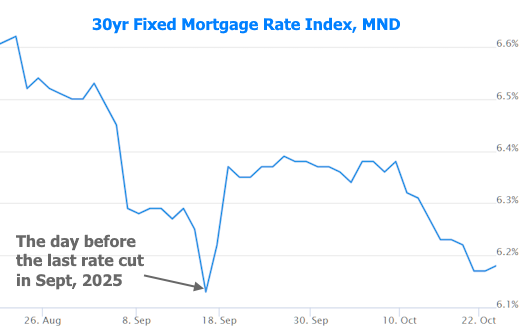

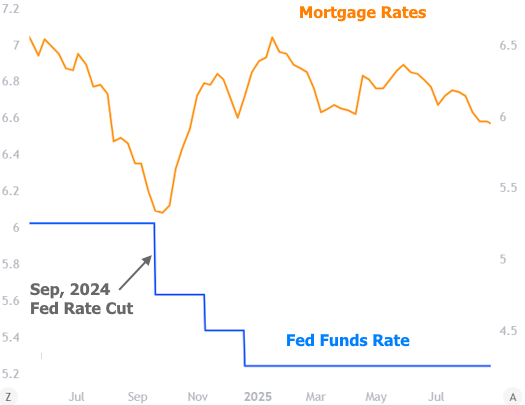

In fact, most of the recent examples involve mortgage rates RISING after the Fed CUTS. September 2025’s example couldn’t be clearer:

Before that, the last time the Fed began cutting rates was September 2024, which also saw a large, counterintuitive reaction:

To be fair, whereas the Fed itself had a hand in pushing mortgage rates higher last month (based on the verbiage of the press conference), 2024’s rate spike had a lot more to do with a shift in economic data. Either way, here’s what matters:

BY THE TIME THE FED CUTS RATES, THE MARKET (INCLUDING THE MORTGAGE RATE MARKET) HAS LONG SINCE GOTTEN IN POSITION.

How does the market know what to expect? Most times, it’s very clear when the Fed will cut based on the tone of comments from Fed speeches and a general understanding of the economic data that informs the Fed’s decisions. The market can actually trade the anticipated Fed Funds Rate via futures contracts.

The following chart shows those rate expectations. In not so many words, the market has been roughly 100% sure of a Fed cut next week ever since the jobs report that came out in September.

Bottom line: any potential benefit for mortgage rates due to the Fed Funds Rate was realized way back in early September. Mortgage rates have moved for other reasons since then because they don’t have to wait for a set schedule to adapt to changing information. Contrast that to the Fed which only meets to set rates 8 times a year, thus often simply delivering what the market had already priced in.

Last but not least: This isn’t to say that Fed Day can’t have an impact on rates, only that said impact would have to come from unexpected WORDS in the Fed’s statement or press conference. The rate change itself is not at all unexpected.

Related Posts