First things first, due to the market's reaction to the Iran war, mortgage rates remain…

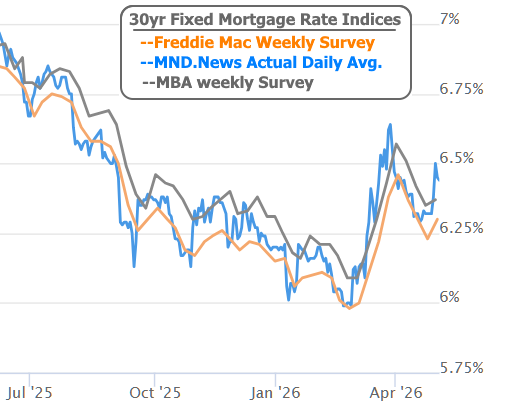

Mortgage Rates Jumped Last Week. The Trend Continues Today

Mortgage Rates Jumped Last Week. The Trend Continues Today

Last week’s newsletter noted an exceptional lack of volatility, but the week ended up shifting gears in a noticeable way.

Monday was actually an extension of last week’s ultra-narrow range. It was Tuesday and Wednesday that did all of the week’s damage. The final two days of the week brought rates a hair lower.

Tuesday’s rate spike followed news that the U.S. was not happy with Iran’s latest peace proposal. Wednesday morning added momentum on reports that the administration met with oil executives to assess the impact of a prolonged blockade on the Strait of Hormuz.

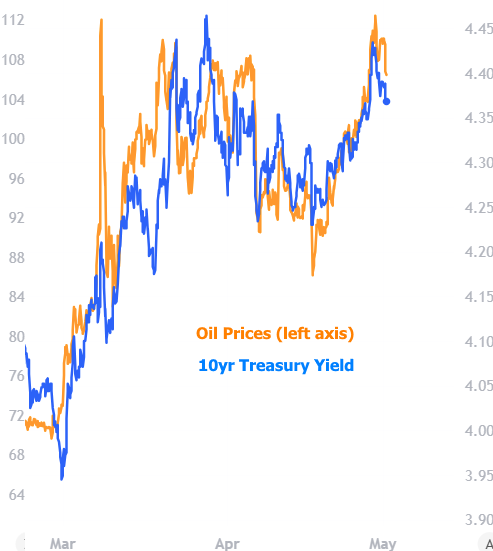

Right from the start, the market impact from the Iran war has been about the free flow of shipping traffic, particularly of oil and other energy commodities. This is why oil prices have continued to correlate so well with bond yields (which, in turn, correlate extremely well with mortgage rates).

By the end of the week, the latest reports suggested some improvement in the prospects for a peace deal, thus the modest drop in oil prices and bond yields seen at the end of the chart above.

Unfortunately, today’s movement has continued the general trend upwards. The overnight and early domestic trading hours brought a mix of familiar and unfamiliar patterns. Up until roughly 8:30am, we saw a very familiar correlation between oil prices and bond yields. Both spiked at 6am following reports that 2 Iranian missiles hit a U.S. warship. Those reports were subsequently denied and oil prices made a full recovery.

The unfamiliar pattern involves bonds breaking ranks with oil to move noticeably higher at 9:20am. There are no obvious explanations in the news or on the data calendar. That basically leaves conjecture. Given the timing, one possibility is that traders wanted to free up cash to “play” in equities markets during peak earnings season. This could also be driven by structural shifts in response to budget concerns. Either way, yields are very close to last Wednesday’s highs (the highest since March 27th).

Powell’s Last Fed Press Conference, But Not His Last Meeting

Last week also brought the latest Fed announcement. There was no chance that we’d see a rate hike or cut at this meeting, so the focus was instead on changes in the Fed’s verbiage, the voting breakdown and the press conference. Markets focused on the fact that 3 Fed members voted against the verbiage of Wednesday’s statement because they feel the Fed should be doing more to acknowledge the risks that rates could move up OR down depending on inflation in the coming months.

Bond yields pushed just a bit higher in response, but more than 80% of the day’s damage had already been done by war-related news.

Less of a concern for markets, but more interesting was the announcement by Fed Chair Powell that he will remain on the Fed board after Warsh becomes the Fed Chair. He’ll be the first Fed Chair to do this since Eccles in 1948. The decision was tied to the fact that the DOJ’s investigation into Fed building renovation costs (ironically, the Eccles building) could still be reopened.

No Jobs Report?

The first Friday of any given month almost always involves the release of the big jobs report–the most important piece of monthly economic data for the bond market. That wasn’t the case Friday, but the market was aware of this fact months ago.

When Friday falls on the first day or two of a new month, and if the previous month had a lower business day count, the BLS (the agency that publishes the data) doesn’t have enough time to do all the required work on the report. In the current case, it will be released next Friday, capping a more active week for economic data and Fed speeches.

While economic data can certainly have an impact, it continues to be the case that bigger, more lasting market impacts are more likely to come from major developments in the Iran war.

Recently Released Economic Data

| Time | Event | Period | Actual | Forecast | Prior |

|---|---|---|---|---|---|

| Tuesday, Apr 28 | |||||

| 9:00 | Case Shiller Home Prices-20 y/y (% ) | Feb | 0.9% | 1.1% | 1.2% |

| 9:00 | FHFA Home Prices y/y (%) | Feb | 1.7% | 1.6% | |

| 10:00 | CB Consumer Confidence (%) | Apr | 92.8 | 89 | 91.8 |

| Wednesday, Apr 29 | |||||

| 8:30 | Durable goods (%) | Mar | 0.8% | 0.5% | -1.4% |

| 14:00 | Fed Interest Rate Decision | 3.75% | 3.75% | 3.75% | |

| Thursday, Apr 30 | |||||

| 8:30 | Jobless Claims (k) | Apr/25 | 189K | 215K | 214K |

| 8:30 | PCE (y/y) (%) | Mar | 3.5% | 3.5% | 2.8% |

| 8:30 | Core PCE (y/y) (%) | Mar | 3.2% | 3.2% | 3% |

| 8:30 | GDP (%) | Q1 | 2.0% | 2.3% | 0.5% |

| 9:45 | Chicago PMI | Apr | 49.2 | 53 | 52.8 |

| Friday, May 01 | |||||

| 10:00 | ISM Manufacturing PMI | Apr | 52.7 | 53 | 52.7 |

Upcoming Economic Data

| Time | Event | Period | Forecast | Prior | |

|---|---|---|---|---|---|

| Tuesday, May 05 | |||||

| 10:00 | ISM N-Mfg PMI | Apr | 53.7 | 54.0 | |

| 10:00 | USA JOLTS Job Openings (ml) | Mar | 6.83M | 6.882M | |

| 10:00 | New Home Sales (ml) | Mar | 0.668M | ||

| Wednesday, May 06 | |||||

| 8:15 | ADP jobs (k) | Apr | 99K | 62K | |

| Thursday, May 07 | |||||

| 8:30 | Jobless Claims (k) | May/02 | 205K | 189K | |

| Friday, May 08 | |||||

| 8:30 | Unemployment rate mm (%) | Apr | 4.3% | 4.3% | |

| 8:30 | Non Farm Payrolls (k) | Apr | 60K | 178K | |

| 10:00 | Consumer Sentiment (ip) | May | 49.5 | 49.8 | |

Related Posts